Today, consumers have greater control over their financial journeys. Therefore, banks must adapt to customers’ evolving needs by providing seamless, end-to-end experiences.

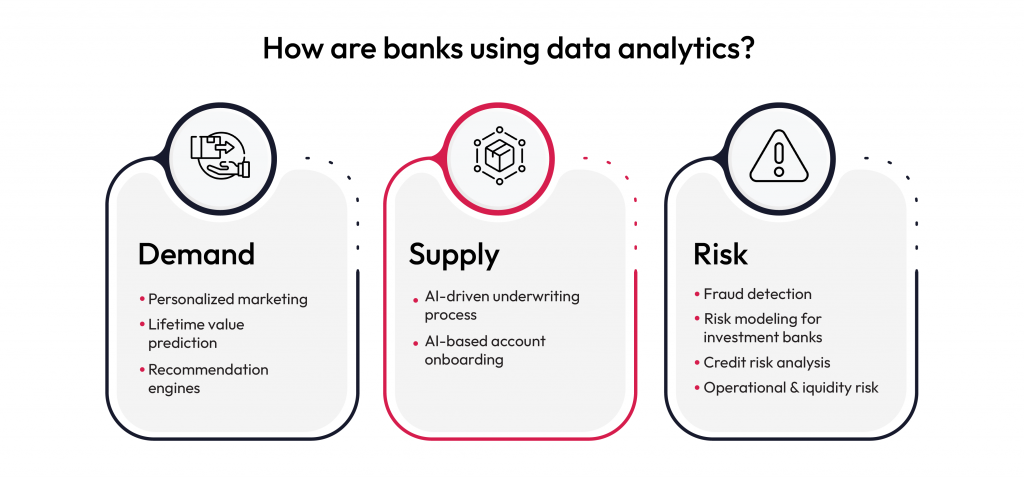

Data plays a critical role in this transformation. Robust data foundations enable banks to efficiently assess transaction details, stakeholder information, payment processing, compliance, and documentation. Given the increasing use of smartphones and the constantly evolving fintech landscape, it is important to focus on addressing three key areas:

Cost reduction

Improved decision-making

Enhanced customer experiences

Now, let’s dive into how predictive analytics can assist in achieving these objectives.

Understanding the role of predictive analytics in modern banking

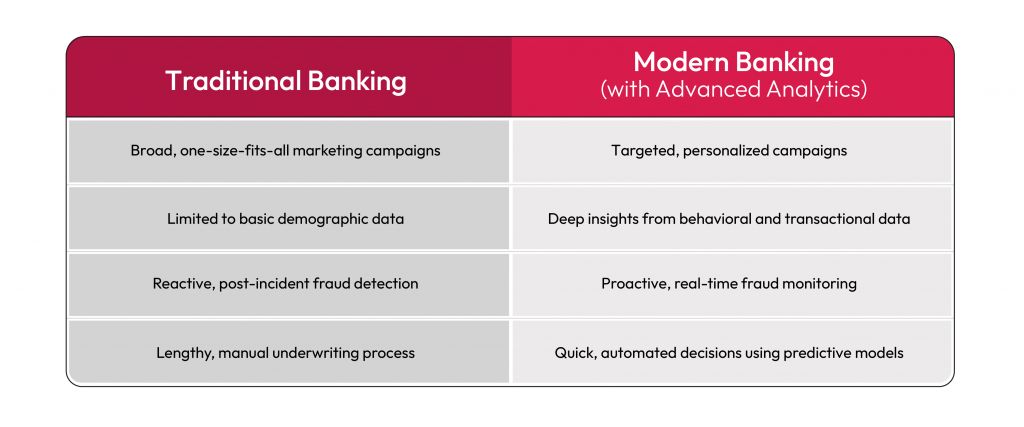

Prebuilt predictive analytics platforms aim to enhance personalization. But these platforms continuously fall short due to constantly changing customer behavior.

Banks need real-time analytics capabilities which helps them understand spending patterns linked to major life or financial events, enabling banks to predict and implement the next best actions (more on this in the next section).

Creating real-time predictive models allows banks to tailor hyper-personalized offers, recognizing the unique motivations behind each customer’s activities and events. This approach ensures more accurate and relevant customer engagement, ultimately driving better results for the customer and financial institution.

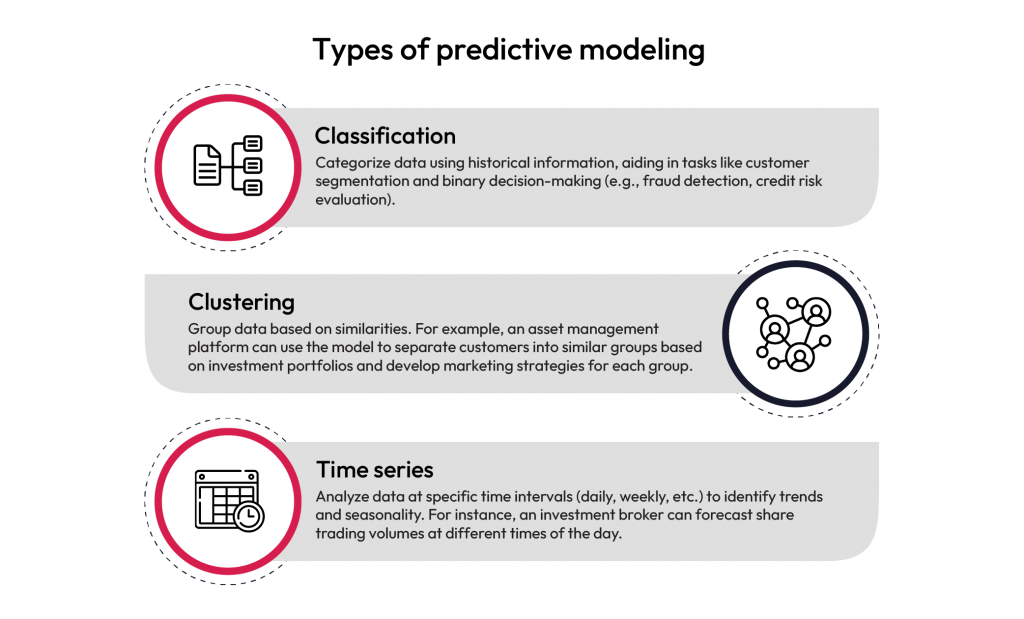

Types of predictive modeling

Predictive modeling automates targeting, minimizing manual data analysis and dependence on human intuition. Here are a few common types of predictive models:

Benefits of predictive analytics

Predictive analytics in BFSI offers significant benefits for leadership aiming to boost profitability and efficiency:

It reduces costs by preventing fraud, lowering loan defaults, and retaining customers who might otherwise churn.

Real-time data updates enable better decision-making, accurately representing risks and boosting confidence.

Hyper-personalization allows targeted customer segmentation and personalized communication, enhancing overall customer experience and satisfaction.

Banks understand the necessity of establishing a top-notch customer experience. However, many still have crucial operational data confined within legacy IT systems.

How are banks adopting experience driven banking?

Banks and NBFCs are embracing experience-led banking by analyzing customer data from digital banking activities, customer interactions, and transaction records. They use transactional, behavioral, and demographic details. Integrating data from both digital and physical channels is crucial for creating a comprehensive customer profile (360-degree view) and omnichannel experience.

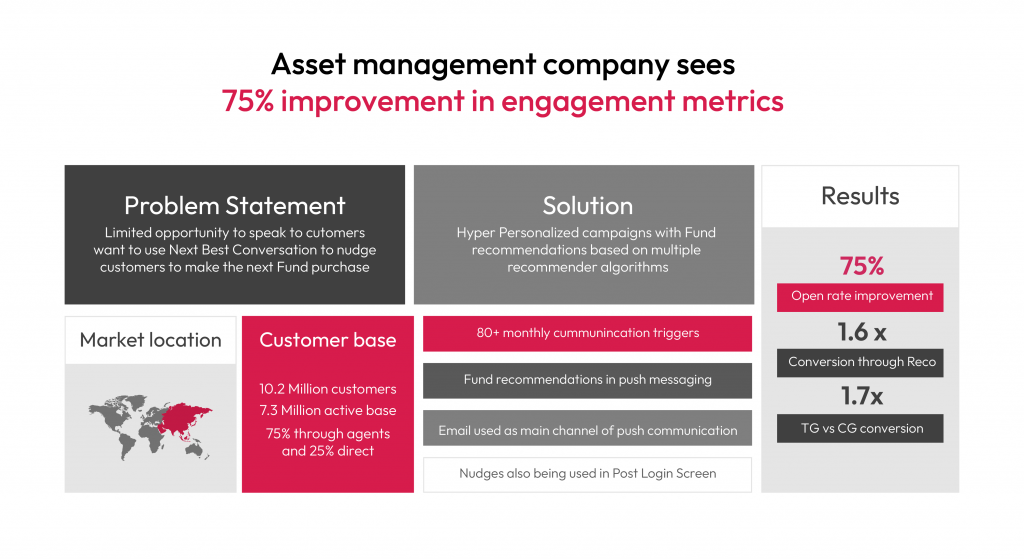

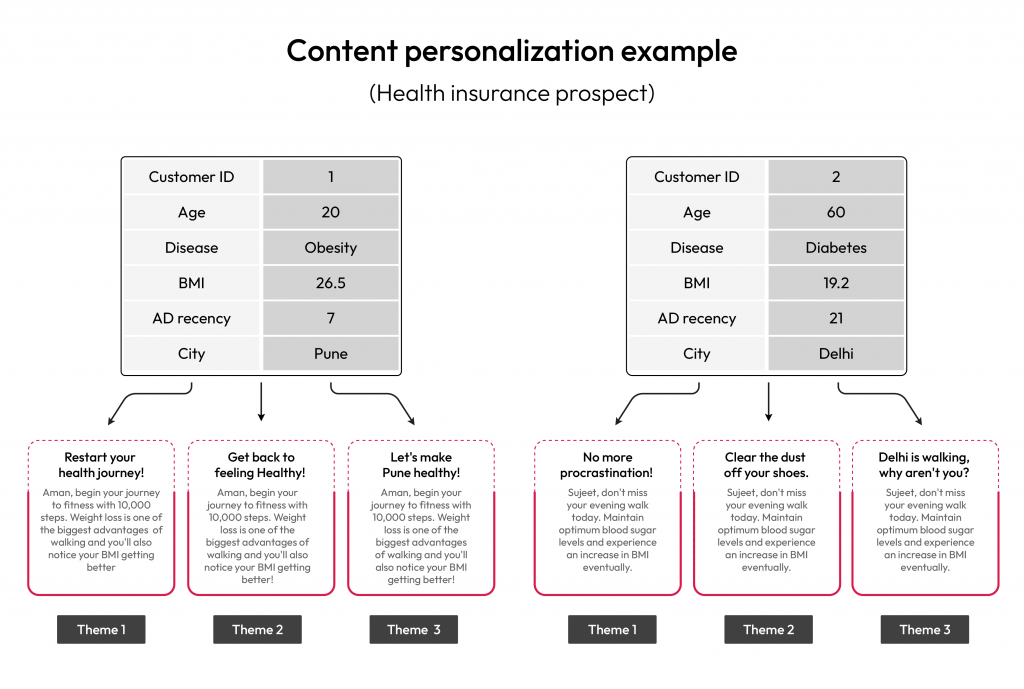

Hyper-personalization is driving a 75% increase in customer engagement in one of our BFSI projects at Robosoft, as shown in the image below.

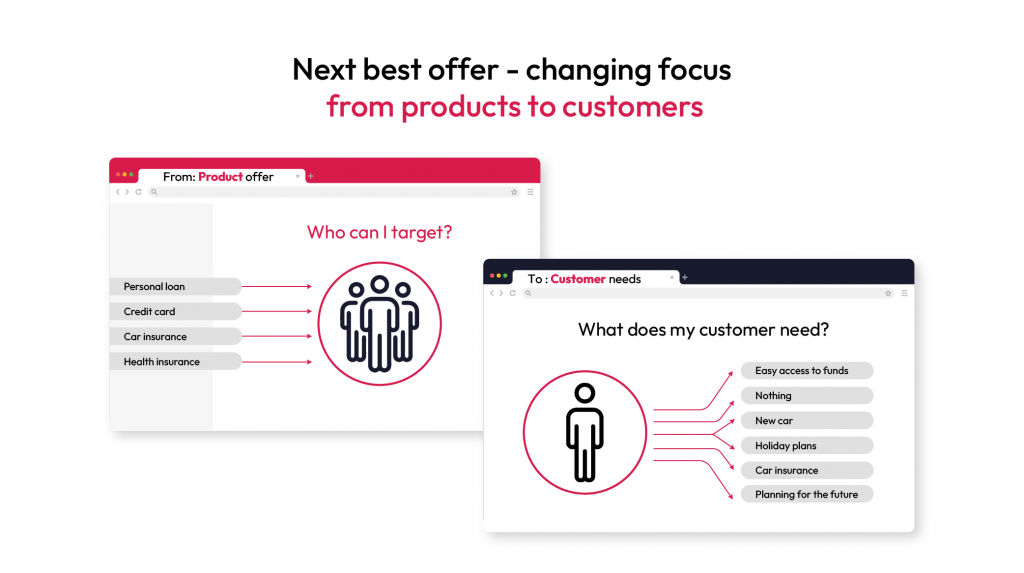

Next best action model

The next best action model (next best offer) uses AI to suggest the most appropriate decision or action for each customer interaction. We have published a detailed blog on building best-in-class recommendation systems – save it for later reading.

In contrast to the past, today’s customer journeys are non-linear and highly dynamic due to frequently changing personal financial situations. Banks can significantly improve results by proactively addressing customer needs with suitable alternatives.

Outcome-driven personalization in BFSI

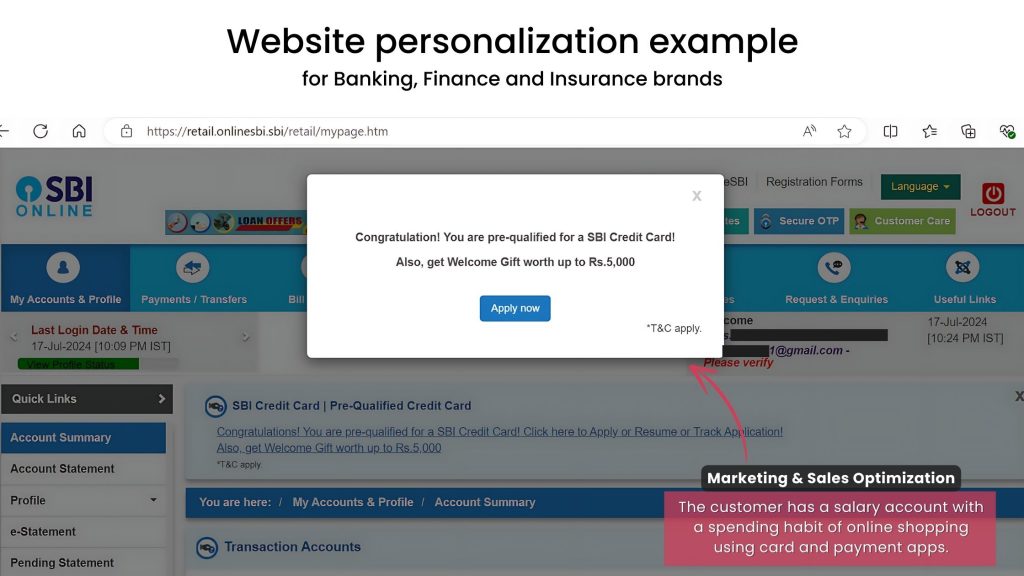

BFSI brands can use predictive analytics to improve website personalization, thereby increasing onboarding completion rates and decreasing drop-offs. Brands can nurture long-term relationships by providing guidance and support during the setup process.

Tailored messages, such as reminders for bill payments, updates on loan qualification, credit card offers, or information about nearby branch locations based on past transactions and browsing history, have the potential to re-engage inactive customers and enhance overall engagement and conversions. Same goes for mobile app personalization.

Use cases of predictive analytics in banking

Collateral management: Predictive analytics helps banks forecast payment flows and anticipate end-of-day and intra-day positions, identifying potential collateral shortfalls. For example, HSBC uses predictive models to improve collateral management, ensuring accurate and timely forecasts to mitigate risks. It leverages NLP and machine learning within its PayMe app to understand transaction intent quickly. Their platform also offers personalized recommendations to customers to reduce irregular activities.

Cash management: Predictive analytics enables banks to forecast cash and manage working capital efficiently. For instance, Bank of America compares a company’s working capital and payment efficiency with industry benchmarks. Predictive analytics provides them with deposit balance notifications, dynamic data visualizations, and metrics for assessing payment efficiency, optimizing supplier payments, managing strategic cross-border payment flows, and protecting against account fraud.

Risk management: Predictive analytics helps take proactive anti-fraud actions, enhance internal audits, and refine credit and liquidity risk evaluations. For example, Wells Fargo bank uses analytics to notify customers about unusually high recurring payments and suggests transferring excess funds by checking savings accounts.

Marketing and sales optimization: Predictive analytics helps banks optimize their marketing and sales strategies by identifying the most effective channels, messages, and offers for various customer segments. For example, HDFC and many other banking players use predictive analytics to segment customers and tailor marketing campaigns, leading to higher engagement and value-building for top customers.

Conclusion

The growing demand for super apps, embedded finance, and personalized services has prompted banks to upgrade their digital banking platforms.

To leverage predictive analytics effectively, banks must update their application environment. Key steps include aligning IT and business initiatives, unlocking core systems, securely integrating data, and optimizing APIs through automation. By following this approach, banks can tap into previously unused capabilities to deliver seamless digital experiences much faster.

Many financial institutions have established AI and machine learning innovation centers to enhance data utilization through predictive analytics. This shift requires building in-house capabilities or collaborating with external tech partner to develop advanced fintech products and tailored digital experiences.

The future of banking lies in seamless connectivity. Like veins circulating blood, banking APIs are now the lifeblood of the financial services industry, allowing diverse financial applications and services to “talk” and transact in real time. Behind the scenes, the Application Programming Interfaces (APIs) drive various convenient functionalities such as account management, payment processing, transaction history retrieval, and third-party financial tools. Today, banks collaborate with Fintech and third-party partners using bank APIs, offering personalized financial solutions and adapting to evolving customer needs.

Banks embracing digital transformation rely heavily on APIs to provide innovative financial services. However, with the increased use of APIs come risks and cybersecurity challenges for banking and financial institutions. As more data is shared through banking APIs, potential data threats and cyber-attacks exponentially increase. So, how can you balance innovation in financial services with banking API security? In this article, we have provided insights into 7 key challenges banking institutions face in protecting their APIs and key API security best practices to bolster security posture.

Key challenges in banking API security

As the financial industry continues to shift towards open banking and API-based solutions, some obstacles to the security of these solutions arise. Here are 7 key challenges in banking API security that banking institutions must address for building secure and customer-centric digital solutions:

Data Breaches and Unauthorized Access

Banking APIs, often interconnected with various applications and services, create an expanded cyber-attack surface. The vast amount of sensitive customer information transmitted via bank APIs can have open-ended vulnerabilities such as unauthorized access and data breaches. Attackers can exploit even minute vulnerabilities to access sensitive customer information, such as their personal data, credit card details, and account numbers.

API Endpoint Security

The security of API endpoints is critical to protecting the overall infrastructure. Malicious actors often target vulnerabilities in API endpoints to launch attacks, such as code injection attack attempts.

Code Injections

On the authentication and validation front, bank APIs must have strong security standards in place to avoid any gaps. Banking institutions cannot afford even the slightest gaps in authentication protocols because such gaps can be vulnerable to code injections by attackers. Using such gaps, attackers may send a script to a banking application’s server via an API request. This may lead to Account Takeover (ATO) incidents and put the application’s internals at risk—it may delete data and plant false information in the application environment.

Encryption and Data Integrity

The confidentiality and integrity of data transmitted through banking APIs are always at risk of attacks if the encryption protocols are insufficient to safeguard data in transit and at rest.

Communication Channels

API transactions are facilitated by multiple communication channels between systems and parties that ensure faster transactions. However, these channels can be vulnerable to security threats like data manipulation, eavesdropping, and man-in-the-middle (MITM) attacks.

Regulatory Compliance

The banking and financial services industry is subject to data regulations like GDPR and PSD2 and security standards such as ISO 27001 to protect customer data and ensure a secure financial landscape. Non-compliance with these standards can result in a more expanded cyber-attack surface on top of severe legal consequences and damage to the reputation of financial institutions.

Brand Reputation

Security breaches that expose sensitive customer data can systematically erode the hard-earned trust between banks and their clientele. The resulting damage to the institution’s reputation and perceived reliability presents financial and existential risks associated with losing competitive positioning grounded in customer loyalty. Therefore, prioritizing robust banking API security via routine vulnerability assessments and continuous authentication enhancements is an investment in maintaining customer confidence and institutional reputation.

10 strategies for tackling banking API security challenges

Banks must implement a comprehensive cybersecurity strategy covering all security aspects to tackle banking API challenges. Here are key banking API security best practices that banks can adopt to enhance their security measures:

Secure API Design

Banks can perform exhaustive threat modeling, risk assessments, and attack surface analysis during API design phases. Identify attack vectors like code injection attacks, MITM attacks, bot abuse, etc. They can architect appropriate countermeasures directly into the API framework with principles of least privilege.

Rate Limiting and Throttling

Banks can implement rate limiting and throttling mechanisms to prevent abuse and protect against distributed denial-of-service (DDoS) attacks. Set appropriate limits on the number of API requests per client or user within a given timeframe.

Input Validation and Sanitization

Banking institutions can adopt a Zero-trust model with input validation and sanitization. They can validate and sanitize all inputs to prevent common security vulnerabilities such as injection attacks (e.g., SQL injection, XSS). Use parameterized queries for database interactions and implement input validation for API payloads.

Logging & Monitoring:

Log all API activities, including requests, responses, and errors, for auditing and forensic purposes. Implement real-time monitoring and alerting to promptly detect and respond to suspicious activities or security incidents.

Secure Coding Practices

Financial institutions can adopt DevSecOps methods with extensive security testing integrated at each API development stage. They can enforce robust coding standards, including proper input validation, data sanitization, and parameterized queries. This protects against common web application security threats like cross-site scripting (XSS) and cross-site request forgery (CSRF).

API Keys and Tokens

Issue unique API keys or tokens to each authorized client to authenticate their requests. Use short-lived tokens and implement token expiration and refresh mechanisms to mitigate the risk of token misuse.

Data Encryption

Employ strong encryption algorithms to encrypt sensitive data end-to-end using standards like AES-256. Banks can implement hashing algorithms like SHA-2 on sensitive data in transit and at rest and apply digital signatures to ensure data integrity. These practices can anonymize or mask any Personally Identifiable Information (PII) data that flows as needed per data privacy regulations.

Web Application Firewalls (WAFs)

Banks can deploy advanced web application firewalls (WAFs) to analyze and filter real-time API traffic. Fine-tuned WAF policies using signatures, anomaly detection, and behavioral analysis can detect and block common attacks like code injection attempts, bot abuse, and DDoS floods.

Regular Security Assessments

Frequent security assessments are crucial to identify vulnerabilities before exploitation by cyber-attackers. Banks must conduct recurring penetration tests, static or dynamic scans, and code audits performed by internal and third-party security teams. This allows the discovery and remediation of flaws like code injection risks, weak authentication, and misconfigurations.

Regulatory Compliance

Banks must maintain compliance with data regulations like GDPR and security standards such as the National Institute of Standards and Technology Cybersecurity Framework (NIST CSF) and ISO 27001 to keep bank APIs resilient to emerging threats.

The banking API security imperative

Maintaining robust banking API security measures is paramount as the banking industry continues to embrace API-driven platforms. Financial institutions can accelerate their digital transformation by utilizing banking APIs while also being vigilant to ensure a robust security posture. By taking the necessary secure API development measures, banks can reinforce customer trust, system resilience, and reputation as stewards of sensitive financial data.

Ultimately, API connectivity promises greater convenience, personalized services, and streamlined banking. However, banking institutions can only achieve this on a foundation of security and compliance first by following banking API security best practices. At Robosoft, we partner with leading banking and financial services organizations across the globe, enabling them to streamline operations and provide millions of customers with secure and seamless digital experiences.

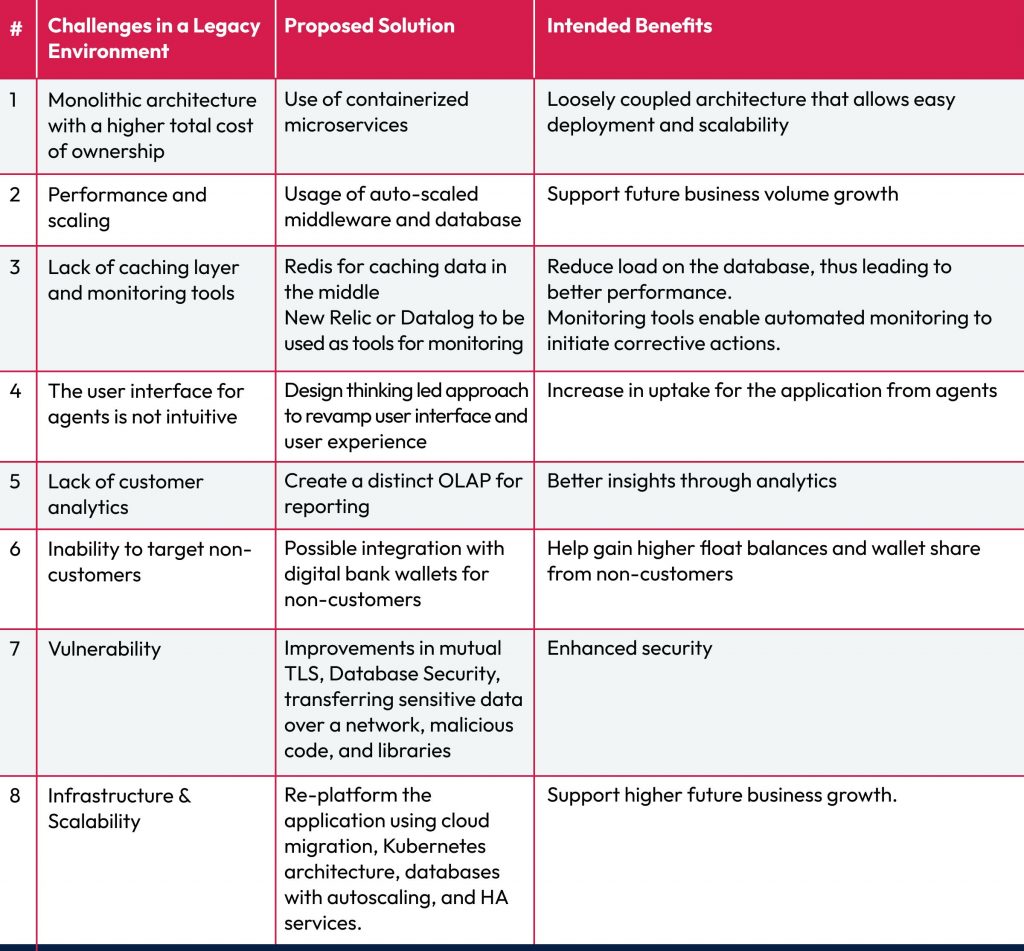

Legacy modernization is the process of transforming outdated business technology systems, known as legacy systems, into modern infrastructure and functionalities. It is the process of updating or replacing outdated software using modern programming languages, software libraries, or protocols and giving a makeover for the digital age. This article outlines the blueprint for modernizing legacy systems and lists key benefits that accrue from this initiative.

Assessment Methodology for Legacy Modernization

The legacy modernization exercise commences with an assessment of the existing application landscape to determine the ability of the existing technology systems (application and infrastructure) to support evolving business needs. A detailed roadmap is drawn up subsequently to complete the exercise. The assessment involves gathering data points around different aspects of the technology landscape. This is supplemented with structured interviews with key stakeholders representing business and technology to understand current pain points and future requirements.

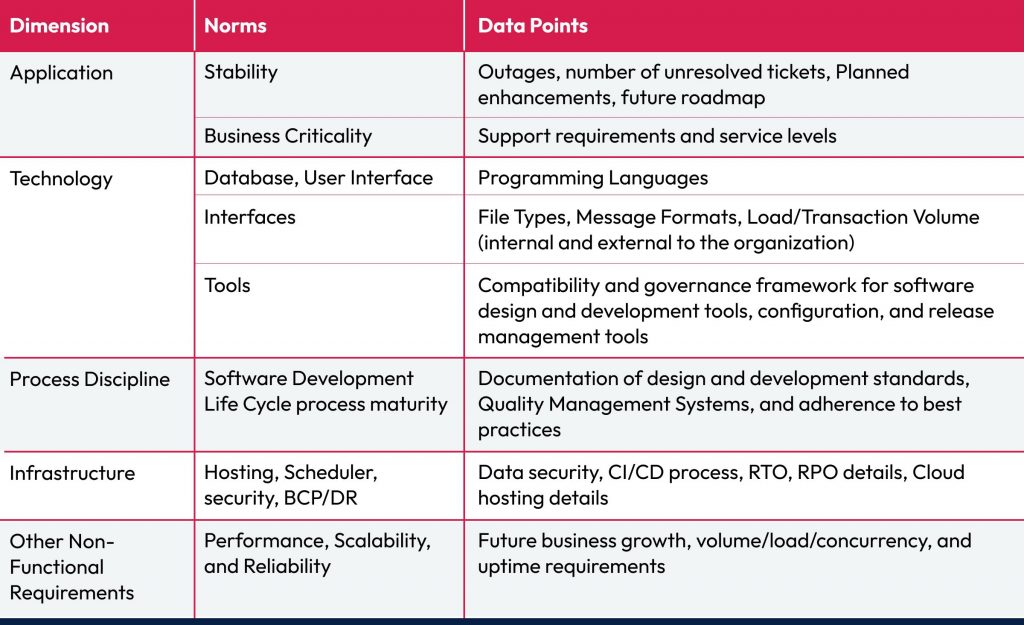

Quantitative Data Points

Quantitative data delves into various platform dimensions, including application stability, business criticality, technology stack, process discipline, infrastructure, and non-functional requirements. Specific data points might include outage frequency, unresolved ticket counts, planned enhancements, technology stack details, interface protocols, data volumes, compatibility of software development tools, adherence to best practices, hosting configurations, disaster recovery plans, and performance scalability metrics.

Qualitative Data Collection

Qualitative data gleaned through stakeholder interviews sheds light on future business goals, technology preferences, regulatory constraints, and pain points. This input enriches the quantitative analysis, painting a holistic picture of the current and future aspirations.

Analysis and Roadmap

Armed with this comprehensive data, we embark on the analysis phase. This involves meticulously examining software code, database structures, and the interplay between quantitative and qualitative inputs. The culmination of this analysis is a robust blueprint for the legacy transformation exercise.

The blueprint addresses critical challenges and proposes targeted solutions, each delivering distinct benefits. For instance, monolithic architectures plagued by high ownership costs can be transformed into loosely coupled microservices, enabling simpler deployments and improved scalability. Performance bottlenecks can be tackled by introducing auto-scaled middleware and databases, paving the way for future business growth. Similarly, implementing caching layers and monitoring tools can enhance performance and operational efficiency.

Benefits of Legacy Modernization

Some of the key benefits are listed below:

Improved functionality and security: Modern technologies offer better performance, scalability, and security features compared to older systems.

Reduced costs: Maintaining outdated systems can be expensive, while modernizing can lead to cost savings on maintenance, licensing, and energy consumption.

Enhanced agility and flexibility: Modern systems are easier to adapt to changing business needs and integrate with new technologies.

Better user experience: Modern interfaces are more user-friendly and accessible, leading to improved employee and customer satisfaction.

Conclusion

Legacy modernization holds lessons for the entire financial services industry. It demonstrates the power of technology to unlock economic potential, empower migrant workers, and strengthen local communities. By embracing innovation and adaptability, financial institutions can thrive in the competitive landscape and contribute to a more inclusive and equitable global economy. By partnering with a reliable and proven digital transformation partner, legacy modernization in one market can inspire and pave the way for similar advancements across the globe, ultimately benefiting communities and individuals.

Wealth management was once the exclusive purview of financial advisors who managed the portfolios of a select, affluent few. Personalized portfolio plans and personal relationships drove such advice. The advent of digital technology has democratized many industries – and wealth management is no exception. As we know, in financial services, digital solutions are at the heart of the consumer experience.

The rise of fintech brands, especially those that help manage investments, is dependent more on technologies than on bespoke human advice, as it is all about scale. This has resulted in redefining wealth management as a service. According to a report by FactSet, investors across the wealth scale—from the mass affluent customer with $100 to invest to the ultra-high net worth (UHNW) client worth $10 million—are already embracing online platforms.

The key to digitalization success is targeting the right business areas, bringing in the right skills, and identifying the key processes to maximize value delivery. A comprehensive hybrid-advisory approach leveraging automation, data analytics, digital, and cloud solutions are the need of the hour.

The Key Pillars of Digital Experience in Wealth Management

Rapid technological advancements, changing investor preferences, and increasing financial awareness are prompting wealth managers to reconsider their customer engagement and business strategies. Digitalization helps modern wealth advisors create and understand their client personas better, moving away from “one size fits all” to a more customized approach. The right technology framework will lower infrastructure costs and improve the efficiency, speed, and scalability of the whole wealth management value chain.

Improving customer prospecting through AI/ML and digital onboarding

Digitalization through AI/ML can help wealth managers identify the right prospects and drive customer acquisitions through data-led personalized marketing. Its ability to combine data from various sources enables it to efficiently classify customer segments based on a variety of criteria, identify prospects using real-time data signals from social media, and generate dynamically personalized content for potential clients, all of which help to increase customer acquisition.

Digital Onboarding: Customer onboarding has traditionally required time-consuming manual documentation. However, many broker-dealers and other wealth management companies are digitizing and automating the process to enhance the client experience and save money.

The foundation for a long-term client relationship is established during the wealth management onboarding process, which includes the first serious interactions between an adviser and a client. Client onboarding processes include

Prospecting

Product selection

Regulatory checks

New Account Opening (NAO)

As a result, businesses are now able to onboard and serve more clients in less time and with fewer resources, maintaining their competitiveness in a market where investors and regulators are driving down fees. Firms with a robust digital onboarding experience will have a solid competitive advantage in the industry.

Achieving investor centricity through data analytics and management

Wealth managers need accurate and real-time data to assess investor sentiments, understand critical market parameters, and produce insights for quick investor decisions. Data can provide timely, pertinent, and actionable insights that can be used to create new (and enhance existing) product and service propositions, optimize channel management, generate higher returns through informed portfolio choices for the investor, and boost customer engagement, and customer retention.

Wealth managers can make wise decisions and appropriate portfolio modifications by using a quantamental investment technique that leverages sentimental analysis, alternative data, and return analytics. Most wealth managers have advanced their client analytics and advisory capabilities and are in various phases of development.

At present, wealth managers have most of their data locked in product silos and legacy systems. Before using advanced analytics, it is understood that access to precise and complete data is necessary. Wealth management companies need a client-focused, precise master data architecture that combines data from all points along the value chain. By increasing their investment in data management and analytics as part of their digitalization initiatives, wealth managers have a better chance of generating higher returns.

Personalized client experience at the front and center

Personalization is one way that advisors can stay competitive with other firms that may offer lower fees or higher returns on investments. According to a survey, investors are increasingly in need of personalized, goal-based planning and other specialized services. In the next two years, 58% of respondents said they would like personalized financial guidance.

Personalization as its name says is unique to each client. To build solutions that will work with whatever position the clients find themselves in, advisors have for decades always thrived on understanding their clients’ backgrounds and perspectives on risk. For instance, knowing information about a client’s household size, state of residency, and annual income are crucial data points in creating customized options that may be more suited for particular people.

Wealth managers can now offer personalized services at a reasonable cost, enabling them to better compete with firms that offer lower fees or higher returns on investments. Automated rebalancing and custom indexing are two examples.

Advisors can automate trading and rebalancing via automated portfolio allocation. And with the help of automated reporting tools, the adviser can inform a large number of clients about portfolio changes.

Enhancing digital investor management and advisory services

For the wealth management sector, it is crucial to offer a more holistic customer and advisory experience. In addition to the human touch, new-age investors are extremely drawn to digital personalization. Wealth managers may increase client acquisition by creating personalized content for potential investors using AI and data-enabled marketing. By increasing customer engagement, a redesigned digital experience can increase customer retention and give advisers more leverage.

A few of the main touchpoints are-

Omnichannel engagement experience: Extends “zero-touch” service by using customized solutions built on video conferencing, on-demand virtual meet (with human advisor), and bot-enabled self-service. Portfolio review and building can be performed over user-friendly virtual solutions accessible over multiple channels.

Data-empowered custom solutions: Includes chatbots and avatars that create a personalized and smoother investor experience, thereby promoting customer retention, upselling, and cross-selling. Many established firms are providing AI/ML-powered offerings to query investor portfolios and their holdings and provide data analytics on the performance of the securities in their portfolio.

Advisor mobile apps: Enables wealth advisors to organize their activities and handle customer interactions. These apps (for example, MyMerrill) can include functionalities like advisor dashboards and 360-degree visualizations of customers and their risk appetites.

Adopting a cloud architecture to improve scalability and operational efficiency

The Information Technology (IT) landscape within wealth management firms consists of legacy systems that maintain a high volume of financial data, which requires increasing maintenance efforts and costs. An increase in financial data will drive automation processes and solutions as automation and AI/ML become more integrated into wealth management services.

Cloud infrastructure can offer a more reliable alternative to internal legacy systems for handling the increased inflow of data at scale, as well as higher operational efficiency and improved agility/time-to-market. By identifying the migration’s decision paths, which will guide the cloud migration strategy through the assessment, design, build, and migration stages, wealth management firms can optimize their existing application portfolio for cloud adoption.

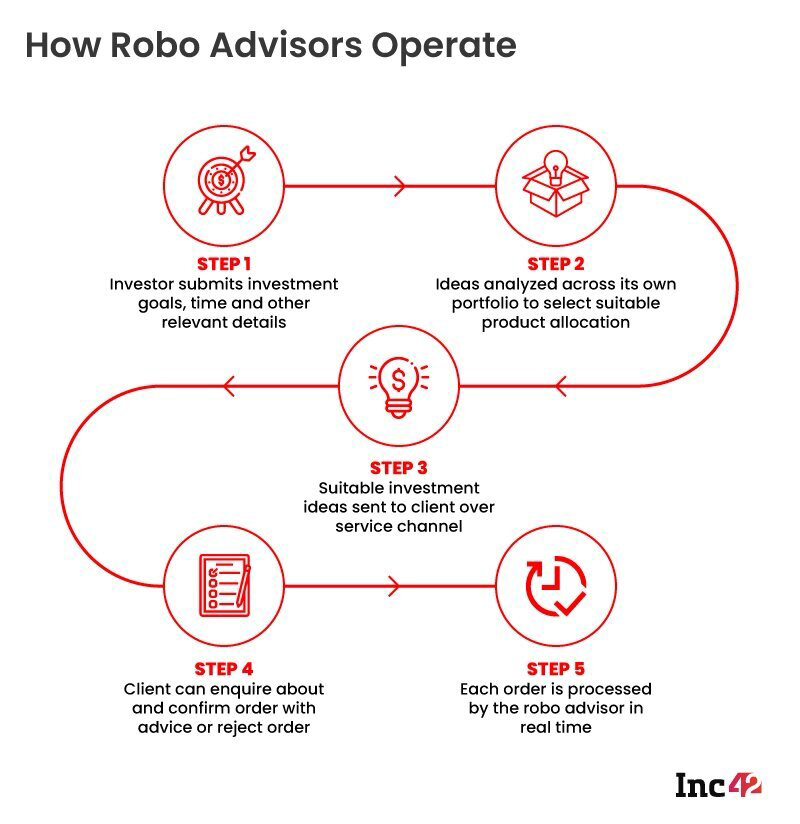

Robo-advisory: taking the stress out of investing

Robo-advisors use automated, algorithm-based systems to provide portfolio management advice. These services are created with customer-centric thinking, and the technology is developed based on their wants and needs.

Customers are drawn to Robo-advice for a variety of reasons. First of all, it entails lower transaction fees and smaller investment requirements. Secondly, it entails more effective investment management. This is because the majority of Robo-offerings offer portfolio management using algorithmically based automated investment solutions that automatically rebalance the customer’s portfolio’s asset allocation without requiring any activity from the user. Thirdly, it provides less experienced investors with more comprehensive advice. Finally, Robo-advice offers more transparency on each investment and how they are likely to perform. The digital interface of many Robo-advisors makes it easy for an investor to analyze their returns versus benchmarks and progress toward goals.

Robo-advice services, whether new-age start-ups or established ones, also have the potential to widen the availability of investment advice from high net-worth individuals to less wealthy investors. Designing robo-advice services for the mass affluent presents a challenge because the customers may have good investment knowledge or little to no investment knowledge, and there is no human advisor there to make sure that the customer has understood the advice they have received.

Robo-advice services that are well-designed assist customers in receiving the best advice for their financial situation and reduce the likelihood that they will purchase the incorrect product. An agile, customer-experience-led, iterative strategy that designs and tests various interaction patterns is the most effective way to do this; whether that be an interactive Web or Mobile App, Chatbot, or combination of multiple technologies, that is right for the persona of a customer using the service.

Enhancing Digital Experience across the Wealth Management Value Chain

Opportunities for digitalization are seen throughout the wealth management value chain. An integrated digital transformation that addresses all the relevant user touchpoints would make it possible for investors and advisers to have a generally improved user experience. Every component of the wealth management value chain can be linked to a digitalization lever (Front office, Middle office, and Back office).

Customer experience is adversely affected by front-office digitalization. The focus is on seamless engagement and improved digital user experience to reduce the turnaround time, increase process efficiency, and ensure a smoother customer journey by Big Tech and Fintech experience.

The middle office, which drives the core line of operation in wealth management, is firmly focused on data analytics. However, given the sensitive nature of client data protection concerns and legislation like GDPR and equivalent laws coming into place around the world, a controlled approach to data management and cloudification is the way forward.

Automation and cloudification are the main digitalization potential in the back office space. The user experience quotient is not very high primarily because the activities are more in-house driven rather than external stakeholder driven.

The Road Ahead

The need to stay digitally connected and have a lasting influence on investors and asset managers have accelerated after the global pandemic. The focus is on creating a digital ecosystem built on tools and measures for a touchless remote experience without compromising on quality, which may have permanently changed how people work.

From a service and product perspective, the focus is steadily moving toward personalization, driven by effective data analysis. The emphasis is now on specialized products, personalized advisory services, and flexible pricing structures for different investment classes. One key factor that unites these shifts is the proactive application of technology and accelerated digitalization, whether inorganically or organically.

Effective use of technology through an omnichannel delivery model is essential for people-centric and relationship-driven industries like wealth management to promote the right level of customer engagement. Firms can look forward to investing in in-house technology and aligning with tech vendors, for the timely implementation of modern investment solutions, keeping relevant to a variety of customer segments, and staying ahead of ever-increasing competition.

In a world of unpredictable yet unavoidable change, individuals, companies and even governments turn to the insurance sector to be prepared. Insurance needs are changing in many ways, such as including risks related to climate change like floods or bushfires, or even novelties like ‘hole-in-one’ insurance (where a golf tournament insures itself to pay the prize bonanza on the off chance that a hole-in-one is achieved). With an increasingly online generation, even as traditional insurers bank on the credibility and trust they have accumulated, the new age InsurTech companies chip away at the market with digital experiences and new models.

When it comes to innovating with technology, InsurTech companies have an advantage over traditional insurers. They are nimble and flexible with their offerings, able to quickly establish low-cost digital platforms and new operating models. InsurTech companies’ biggest advantage is the hold they have over the customer’s pulse. With smartphones becoming commonplace, customers find that InsurTech offers comfort, convenience, and speed in making important insurance-related decisions and transactions.

Research indicates that 28 of the 280 FinTech firms that have turned unicorns to date have played an instrumental role in driving innovation or disrupting the way insurance is done. From claim management to reinsurance, asset management, customer onboarding, and engagement, InsurTechs have earned their colors across the insurance value chain and are here to stay.

Challenges to InsurTech

Despite these gains, experts believe that InsurTech market growth will have to endure several constraints. Foremost among them is a lack of awareness about the value InsurTech can deliver, and dearth of professionals who can expertly work with advanced technologies. These factors could restrict InsurTech companies from scaling their technology capabilities to the extent desired.

However, it is undisputed that the future of insurance will be tech-driven in the form of embedded ecosystems, AI & ML, blockchain, low code technology, and more. 85% of insurance companies recognize the need to prioritize digitalization, so it may not be long before traditional market leaders catch up with their technology capabilities or look to buy out smaller players. InsurTech start-ups have their work cut out in gaining the kind of trust and credibility enjoyed by established insurers. Now, they must rethink strategy to retain their technology advantage.

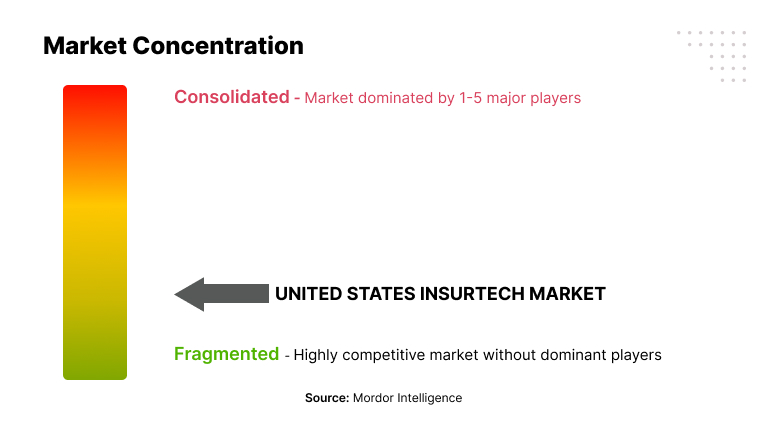

If we look at the US which is the global market leader, InsurTech is expected to grow at more than 7% CAGR over the next five years. The competition is definitely heating up here.

Business opportunities for insurance will continue to flow in as the world becomes increasingly digital. More aspects such as health, travel, auto, and home will be included under the umbrella of online insurance.

InsurTech companies will need rely on their strength – technology – to offer a wider, more personalized range of benefits shaped by data, new offerings like social insurance, and cost saving tools like virtual agents powered by conversational AI etc.

McKinsey research opines that five rapidly advancing technologies will significantly redefine the future of insurance. These include applied AI, distributed infrastructure, future of connectivity, next-level automation, and trust architecture. By putting the full force of their tech advantage here, InsurTech players can solidify their business and expand their portfolio.

Take for example, the AI-enabled platform offered by Bdeo, available on their mobile app. It comes with a chatbot that uses Natural Language Processing principles to liaise with claimants, get first-hand info on the accident/damage that has occurred and helps them share photographic evidence of acceptable quality on the platform. The insurer can use the app to inspect and investigate the incident remotely using computer vision models. Doing so helps avert errors in evaluation and improves the overall claim processing experience for both the insurer and claimant.

Studies predict that AI will disrupt underwriting, claims, marketing, distribution and other core processes by enabling more human-like interactions across various customer touchpoints. There is a plethora of opportunities that can be exploited. For example, the associated customer data can be used for predictive analysis and forecasting, which can in turn, inform the development of new product and service lines.

2. Enabling intelligent insurance with distributed infrastructure on the cloud

Many core insurance processes that have been weighed down by legacy systems are finally modernizing. This allows insurers to leverage cloud-native infrastructure, ramp up to manage workloads without impacting customer experience and speed up their innovation efforts. Thanks to cloud computing, they will be better placed to harness the massive amounts of claim-related data available to benefit their customers and increase profitability.

This is a huge opportunity for traditional insurers to collaborate with InsurTech to form partnerships that leverage their strengths and quickly enable plug-ins, distribution channels, and other value-adds. For instance, InsurTechs can offer digital solutions to efficiently sift through vast historical data of established insurers, to identify and interpret customer patterns and insights to determine the kind of new product/service lines to be developed. In fact, at least 75% of insurers were found to be seeking out InsurTech collaboration to improve their customer experiences according to a Capgemini survey.

3. Developing insurance products using telematics

Telematics technology is increasingly being used to monitor, interpret, even influence consumer behavior. For example, innovation stimulated by IoT adoption is being applied in connected home devices to track humidity, temperature and other parameters, which potentially cause damage to property. Insurers can leverage the data generated on these devices to estimate risk over time. Similar innovations are being explored across the domains of insurance to life, health, auto, manufacturing, commerce etc. The advent of 5G will enable real-time data sharing and make it possible for insurers to turnaround services faster than ever.

For example, being covered against ride cancellations is a value-add for customers and digital solutions can be developed to enable this as a timely service using real-time availability of data. Another example of value-add is the coverage against bodily harm to earners and riders of every trip offered by Uber in partnership with a leading insurer.

4. Enabling human decisions via bots

While robotic process automation (RPA) has proved its worth in automating back-office functions in the insurance industry, there’s a lot it can do in terms of next-level process automation that will shape the future of insurance. For example, the IoT-enabled, real-time monitoring of factory equipment can predict maintenance needs and prevent repair or damage that result in insurance claims.

RPA also has a distinct role to play in supporting human decisions in a cost-effective and timely manner. As an example, it can expedite claims processing wherein photos of the damage to a vehicle are automatically assessed and verified for authenticity without requiring an in-person visit by a claims adjuster to the damage site. Likewise, building optical character recognition features into RPA will help extract text from claim applications in large volumes and ensure that the information it contains is distributed to the right functions for further processing.

5. Laying the foundations for trust with blockchain

Increased digitalization of insurance is raising security concerns due to the sensitive nature of customer data that is being shared across the insurance ecosystem. Building customer trust will be a priority for insurance players, which is where blockchain comes to the rescue.

Along with its advantages of transparency and efficiency, blockchain will play a leading role in helping carriers safeguard customer data from cyberattacks and data breaches. It will also simplify user authentication, identity management, and fraudulent claim detection etc. Through blockchain-based smart contracts, policies can be converted to decentralized lines of codes that will make consumer’s data immutable and easily available for immediate verification in the event of any claims made to the insurer. If it proves to be fraudulent, the contract will immediately be discontinued, and the premium amount paid returned to the insured. This kind of data transparency and responsiveness of the system will help build trust between all concerned parties.

The future of digital insurance paved by tech-led design

As insurance becomes more digitally driven, user experience (UX) will be all the more crucial for branding. While an omnichannel insurance experience is the norm today, creating memorable user experiences at all possible touchpoints will be paramount to carving out stronger market positions for the InsurTech brand.

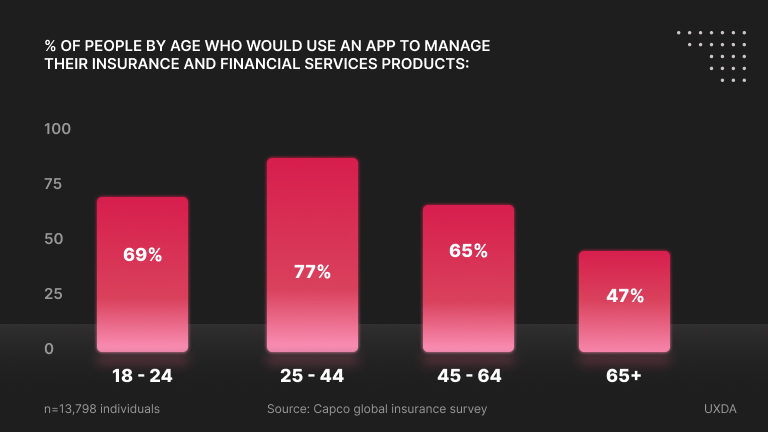

For example, the silver agers generation are no longer the most dominant consumers of insurance. In fact, studies that the interest now being shown by millennials and Gen-Zers towards insurance products exceeds that of the older generations.

Or, as this chart indicates, nearly half the individuals in the 65+ age category are unlikely to use an insurance app. If the insurer wants to attract more consumers from this cohort, they will need to leverage data to understand preferences, simplify interfaces, customize their offerings and so on.

According to the World InsurTech Report 2021, half of the insurance customers are willing to explore solutions offered by new-age digital players. The insurance market will experience disruption and a new order will emerge. Traditional insurers are more likely than ever to engage in partnerships with InsurTechs to stay relevant. Niche players and start-ups in InsurTech will not only need to leverage emerging technologies but also understand the complexities of insurance better and closely follow changing needs of their target demographics.

Led by research, data analytics, and empathic and intuitive design of user-centric interfaces, InsurTech players will be able to create market differentiation that can help them explore opportunities to build partnerships with traditional players so that both survive and thrive.

Taking a loan to pay for higher education is a common phenomenon in the US. But who would have imagined that due to food inflation, even essentials such as groceries will be considered for the ‘Buy Now Pay Later’ (BNPL) phenomenon? On Klarna, a leading player in this domain, more than 50% of the top 100 items bought on the app belong to grocery or household items.

As more younger consumers go online, they have been experimenting with alternative payments methods. The rise of smartphones and e-commerce, now integrated with social media platforms is among the top trends impacting online sales and payments. The creator economy too is fueling social commerce. Such trends have attracted a new demographic – the millennials and teenagers. Now wonder that Fintech players are crafting new solutions to meet this demand. Pre-paid cards and digital bank accounts for teenagers are meant to address this trend. Fampay, Junio in India and Revolut <18 in the UK are a few examples.

BNPL: ‘credit’ where due

Over the last couple of years, the BNPL trend also referred to as ‘Pay in 4’ model, is meant to address a market opportunity. The post-COVID scenario and inflation in many countries has made it even more attractive – especially for a demographic with limited income resources.

In a 2021 research in the US, it was found that 60% of those surveyed had used a BNPL service. The main incentive of course is the interest-free instalment option which reduces the spending pressure and provides an incentive for online purchases. Klarna, claims a 41% increase in order value and 30% increase in conversion through their BNPL solutions.

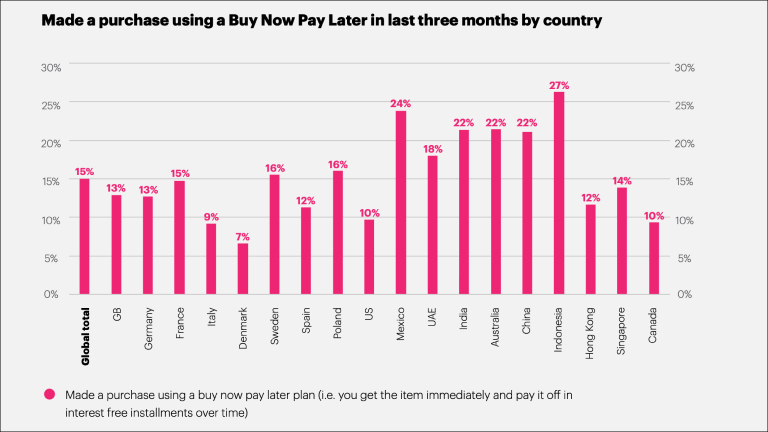

The adoption of BNPL is a worldwide phenomenon. According to research in 18 countries from YouGov, Indonesians made the highest proportion of purchases using a BNPL plan (27%) – almost double the global average of 15%.

The same survey also mentions that in India, BNPL services grew a mind-boggling 637% in 2021. Naturally, such solutions are popular among the younger demographic. A whopping 75% of BNPL users in the US are Gen Z or millennials. Credit card penetration in India is still in single digits. BNPL was seen as the answer to a demographic which could be denied a credit card.

Fintech brands too were quick to spot the opportunity. In mid-2021 there were already 50+ companies offering ‘Buy Now Pay Later’ services across the world. The number is likely to have gone up in the ensuing period. In India, brands such as UNI have positioned themselves as a revolution in credit offering payment options in three or two instalments.

BNPL players are also tying up with large retailers such as Amazon, Macy’s and Target – thereby gaining access to a large, ready customer base. Aside from the smooth user experience, some serious technology is at play behind BNPL experiences. Apparently, Affirm uses over 200 consumer data points for risk management, while its existing loan users improve its AI algorithm.

Some of the aspects BNPL players must pay attention to, from tech POV are:

Infrastructure: The cloud infrastructure should help scale up operations easily, provide new products and services using on-demand computing. It should also safeguard consumer data and aid in maintaining regulatory compliance.

Risk Management: machine learning comes into play here in developing models for better risk identification and management, real-time credit score prediction, and payment management.

Security: BNPL players are expected to maintain the essential infrastructure in accordance with security standards. Major players such as Klarna collaborate with AWS’s compliance and security assurance teams.

Analytics: The integration of data workflows should make it simple for data to be absorbed from a variety of structured (such as transaction and payment history) and unstructured sources (such as social media activity, credit bureaus, and spending behavior). Such information gives early warning signs of credit degradation during times of difficulty and assists in the creation of a 360-degree perspective of the consumer. The data analytics tools aid businesses in understanding the preferences of their customers and the performance of their own products.

Tech partners: to create better products and solutions, fintech companies merge or partner with services who add value. Block (formerly Square) acquired Afterpay a pure play BNPL company. To enhance its underwriting capabilities and speed up automated credit decision making, particularly to draw in millennials and Gen Zs, Klarna purchased the Italian payment business Moneymour. Additionally, Provenir, a provider of credit risk analytics, and Klarna have teamed up. Credit scoring, underwriting, and real-time decision-making at the point of sale are bundled as a result of their combined efforts.

So does all this point to a rosy future for BNPL? According to industry experts it may be prudent to exercise caution as regulators have taken steps affecting the business model of several players, in markets like India. What’s driving such actions is the fear of triggering overspending leading to credit risk and worse still, poor financial discipline among a young audience.

Buy Now, Pain Later?

In June 2022, the Reserve Bank of India issued a circular banning non-banks from loading pre-paid instruments (PPIs) such as digital wallets or cards using credit lines. Several brands suspended their BNPL offerings following this development. According to Euromonitor:

The Financial Conduct Authority (FCA) in the UK has named the key risks the model holds for consumers and the wider credit market. These include, but are not limited to, the lack of information for consumers around the features of BNPL, the lack of consumer creditworthiness assessment, and the potential creation of over-indebtedness.

Nearly 70% of BNPL users admit to spending more than they would if they had to pay for everything upfront, according to LendingTree. What’s more, 42% of them have made a late payment on them. While consumers maybe attracted by simple onboarding experience and ease of payment, the offline experience has not always been pretty in India. According to reports, lending apps have used unsavory methods to coerce users who have defaulted on payments.

These developments point to the industry being regulatory dependent in the near future and rightly so. What could be the broad contours of solutions for both end consumers and Fintech players? According to financial industry insiders, full-service banks seem to be better placed to make the most of the real demand for ‘pay-over-time’ services. Pure-play BNPL service providers may have to tweak their core offering based on the regulatory oversight in their home markets.

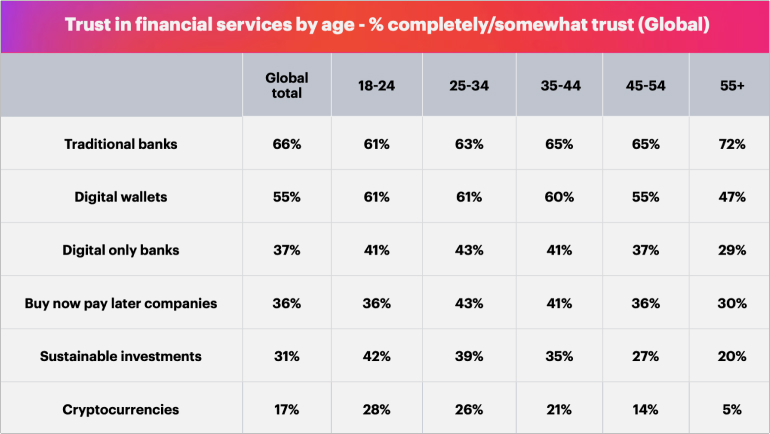

Trust, convenience and ease of use are three critical aspects of BNPL success. Traditional banks score better on trust – a critical factor in financial service products. According to YouGov study, only 36% in the 18-24 age group trust BNPL companies as compared to 61% in the same group for traditional banks.

There are several pointers for both end-consumers and the fintech ecosystem from this emerging trend.

Brands in the BNPL sector have a real obligation to educate users about financial prudence, especially to the younger demographic. It must be made clear to the end-user in every touch point that this is a loan and there are consequences for missed payments. Consumers must also be educated about the risk of over-spending and its fallouts. This is important as a key metric for BNPL players is the re-use of a service. According to PayPal 70% of their customers use the service within six months of first use. In the US, as BNPL is offered at more merchants the older demographic too is coming into the fold. So, it’s not just the Gen Z’s and millennials who will be target audience in the future.

For brands, convenience could translate to ubiquitous acceptance across online portals and POS at physical locations. Clubbing all BNPL payments with one brand would also make it easy to manage for the end user. Ease-of-use comes into play with respect to the app experience. The onboarding should strike a balance between being friction-free and conveying the details of the financial terms in a transparent manner, especially the repayment schedule and penalties for delay.

In sum, BNPL is a useful and convenient product feature especially for those with limited leeway in upfront spending capacity. But industry growth aided by great digital experience will depend on regulatory constraints and educating the consumer about the need for financial prudence.

Founded in 1472, Banca Monte Dei Paschi di Siena is said to be the oldest surviving bank in the world. Since then, the banking industry has come a long way. It has not only grown in size but also wields huge influence across the world. Several powerful local and global brands have been established and many of them are synonymous with trust and financial safety. But as with every other industry, change is the only constant in banking too.

The onset of the internet, smartphones and better mobile connectivity has given rise to digital banking. For a large set of customers there was no reason to visit a brick & mortar branch office as all transactions could be completed on the web or on the mobile. Over the last few years, the term neobank has been used to describe digital-first or digital-only banking services. Europe, India and the US have been home for several successful neobanks in the recent past. What’s more, as a sign of its popularity, several niche services have already been launched in the domain:

– Launched recently, Lucy is a neobank targeted at women entrepreneurs.

– There’s a neobank exclusively to meet the needs of musicians: Nerve merges user experience and financial technologies to help artists build stronger communities and sustainable careers.

What makes neobanks an attractive proposition for consumers? Let us attempt to answer a few basic questions about neobanks, the reasons for their popularity and the role of digital experiences.

1. What are neobanks? Are there different types of neobanks?

When banking began the digitization journey, the FinTech industry emerged, providing technology to digitize several processes in financial services. This enabled online banking, payments and other services like insurance and wealth management. Customer preferences shifted as they embraced the convenience of online transactions. They prioritized convenience over the traditional approach of trusting a person at the local bank branch or an insurance agent. They preferred digital payments over cash, removing the need for ATMs. Neobanks emerged at the intersection of technology and banking in this industry shift. The concept of neobanks emerged around 2015, and in a very short span of time disrupted the entire banking industry.

“Neobanks are digital first, born in the cloud, completely online banks, with absolutely no physical presence. They provide banking services only via web or mobile a smartphone app.”

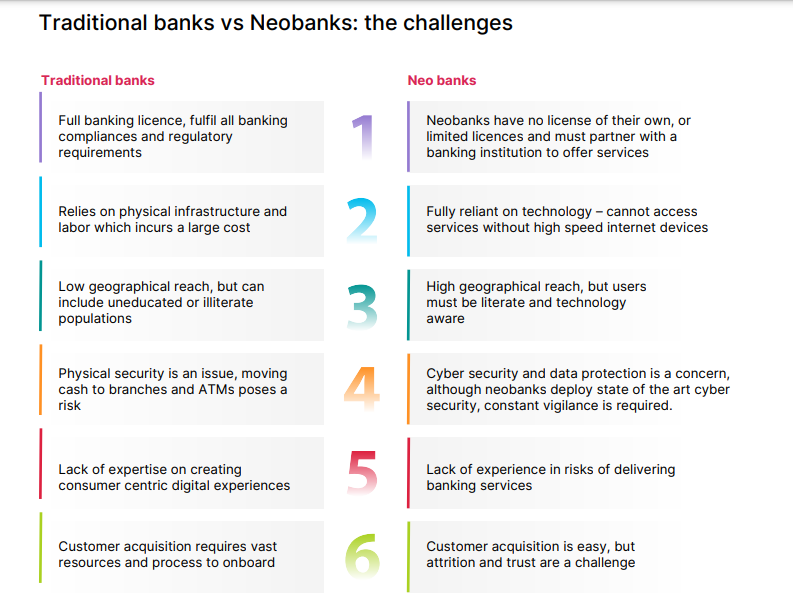

In Europe and the US, neobanks are also referred to as ‘challenger banks’ or ‘open banking’. They all have the following key characteristics: – Customer first: understanding the generation that are digital natives, and rely on their phones for everything, neobanks adopt an entirely digital approach to the customer experience, offering crisp, user friendly and intuitive interfaces. – Technology powered: Neobanks are entirely technology driven, using technology to acquire customers and deliver services. They deploy artificial intelligence to create personalized, customized offers based on data. Traditional banks rely on in-person or phone customer service, while neobanks may rely on chatbots or Robo-Advisors. – No physical presence: Neobanks have no physical presence at all; they operate without branches, offices, ATMs or any type of physical infrastructure. – No banking license: Neobanks typically do not have a banking license and offer services along with a banking partner, although some countries that allow digital banking licenses have seen some licensed neobanks.

In general, a neobank is different from a traditional bank, a mobile wallet or a digital bank, and can fall into these categories.

1. Independent neobanks that work with banking partners: most neobanks follow this model, where a FinTech firm creates a digital experience with a mobile or web platform, and they collaborate with conventional banks to offer services and products. Yolt, Lunarway, and Moven are examples of neobanks that work in this model.

2. Neobanks owned by traditional banks: several traditional banks have realized the value of a digital-only, customer first approach. Aside from their online banking portals, banks set up wholly owned neobanks as part of their digital initiatives such as DigiBank set up by DBS.

3. Licensed neobanks: some countries such as UK, Brazil, Germany, South Africa, and Singapore allow digital banking licenses, and as a result, some neobanks have acquired banking licenses. This allows them to offer more valuable, regulated services. Monzo, N26, MyBank, Starling Bank, and Revolut are some examples.

2. Aside from lack of physical outlets, how are neobanks different from traditional banks?

What neobanks did best is understand the new age consumer and use technology to create a user-first banking experience, rather than a regulation and process first banking experience.

Neobanks create a purely delightful digital journey with easy to use and attractive interfaces. New solutions are built based on a mobile-first experience over a branch-first experience. They use data to create unique solutions and understand the pulse of the customers to create digitally enabled experiences.

3. What aspects of neobanks do customers like?

It is believed that the incredibly easy account opening and smooth, quick on-boarding are hugely attractive to those who have signed up with neobanks (Niyo in India anchors its advertising on the fact that its account opening takes just 100 seconds).

Deloitte surveyed millennials in over 20 countries and found that 68% say that new financial players understand their needs. They expect banks to offer a slick and sophisticated app, with new offers tailored to their needs. 79% of millennials access their mobile banking app multiple times a week. With Gen Z entering the workforce, there will be new expectations of social media integrations and deeply unique experiences.

Consumers want fully connected services from neobanks, which means creating products and services that cross over the traditional industry lines.

– Hyper-personalization options such as bundling services like real estate with home loans, peer to peer payments, personal finance planning, and even lifestyle related features are being integrated into the digital experience.

– For small and medium enterprises as well, neobanks are offering integrated services of banking as well as financial management including accounting, invoicing and taxation.

Neobanks have seen widespread adoption and growth as they are agile and easy to set up, and customers find it simple to engage with them.

Easy account creation: customers can easily open an account in a few clicks, without having to visit a bank branch or provide reams of documentation.

Personalization: the user experience is unique and tailor-made with data available on spending patterns and other insights

Range of services at lower fees: not having to bear costs of labor or branches as well as less spend on regulatory compliances allow Neobanks to offer services including banking, debit and credit cards, forex, loans and others free or at very low service rates

4. What’s in it for neobanks?

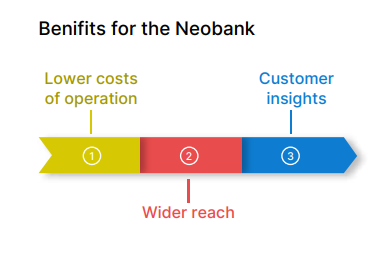

Low cost and agile: Neobanks are 100% online, so they have no investment on physical infrastructure and low operational spends such as customer support, ATMs or bank branches.

Wider reach of customers: the ease of account creation via mobile phones and simple user interfaces, enable neobanks to reach the unbanked populations including small and medium enterprises, blue collar workers and youth.

Data on consumer patterns and trends: being completely digital allows neobanks to collect and analyses consumer data, understand the patterns, and behaviors. Using machine learning allows them to provide a customized experience, and artificial intelligence helps neobanks create personalized services.

5. What is the industry shifts which were favorable to neobanks?

Digital acceleration: The pace of adoption of new technologies and relying on digital solutions for everything (be it ordering food or hailing a cab) increased recently. The pace of this change accelerated after the Covid-19 pandemic and has impacted several industries including media & entertainment and delivery services.

Hyper-personalization: Product or service parity is common across categories. While consumers may see very little difference between brands, the ones which cater to a ‘segment of one’ are bound to have an edge. Consumers expect unique services, ongoing communication and access to relevant information and data.

Change in the notion of trust: An imposing building and presence over decades was equated with solid performance and trust by the older generation. Millennials and Gen Z don’t see such as markers of trust. They expect the digital experience to work and work best for them.

Shifts in technology capabilities: The foundational elements of technology put in place in the first wave of digitization by banks and FinTechs have a lot to do with the success of neobanking. API integrations allow data and information to be shared by various applications, which allows neobanks to offer simplified services, and fast digital experiences. Account aggregator system reforms such as India’s UPI (Unified Payments Interface) have enabled ways to connect, bypass legacy-infrastructure hurdles, and innovate using technology.

Technology-enabled design as brand edge: Both B2C and B2B enterprises have come to accept that design can be a secret weapon in creating brand affinity. While slick user interfaces attract users and simplify the digital journey, machine learning and artificial intelligence are bridging data and user experiences. With these AI / ML applications, neobanks draw from individual data to create a personalized experience, or offer unique services or products by predicting a user’s need.

Despite the rise of neobanks, traditional banks which have adapted well to the digital world still have an edge due to brand recognition, positive equity and a huge customer base. All in all, it promises to be a win-win for the end consumers who can get the best of banking facilities, customer service and digital experiences.

The success story of Asia’s FinTech industry is something that the rest of the world is now trying to emulate. FinTech in the US is just beginning to catch up, especially after the pandemic hit and digital channels became a necessity. This Economist article suggests that in the US the volume of transactions on PayPal was 36% higher in March 2021 than last year. The number of people using Square’s digital Cash App rose by 50% to 36 million during 2020. While the FinTech market in the US is growing, it is yet to achieve the scale and maturity that the Asian markets have achieved in the last few years.

Asia is a hub for some of the most advanced FinTech markets and it continues to be so. A recent EY survey shows that Asia has retained its global leadership in FinTech adoption this year too. FinTech adoption in Asia-Pacific markets has grown enormously in the last two years. Markets like Hong Kong, Singapore, and South Korea have seen a consumer adoption rate of 67%, but China and India are spearheading the FinTech growth and are at close to 87% adoption rate.

Factors responsible for this accelerated growth and adoption include consumer demand, market-friendly government policies, high mobile penetration, and reliable internet infrastructure. The rise of Super Apps is also one of the most important aspects that have led to Asia’s FinTech growth.

Here are some of the key trends from the Asian FinTech landscape and what they could mean for the rest of the world.

Rise of Neobanks or Digital-Only Banks

Neobanks are online-only banks and do not have any physical branches. In the present context of the global pandemic, it is only natural that neobanks have become popular. However, aside from the pandemic, the other factors that have fuelled the popularity of digital banking in Asia are:

A large unbanked population got access to credit and essential financial services at lower costs through these FinTech players.

The ASEAN population is primarily young, and Neobanks are especially appealing for younger people who don’t want to go to the physical branches.

The governments and regulatory agencies support the digital movement in these areas. In 2019, regulators in Hong Kong issued eight digital banking licenses. Singapore has also granted some digital banking licenses while Malaysia and the Philippines are opening up applications gradually.

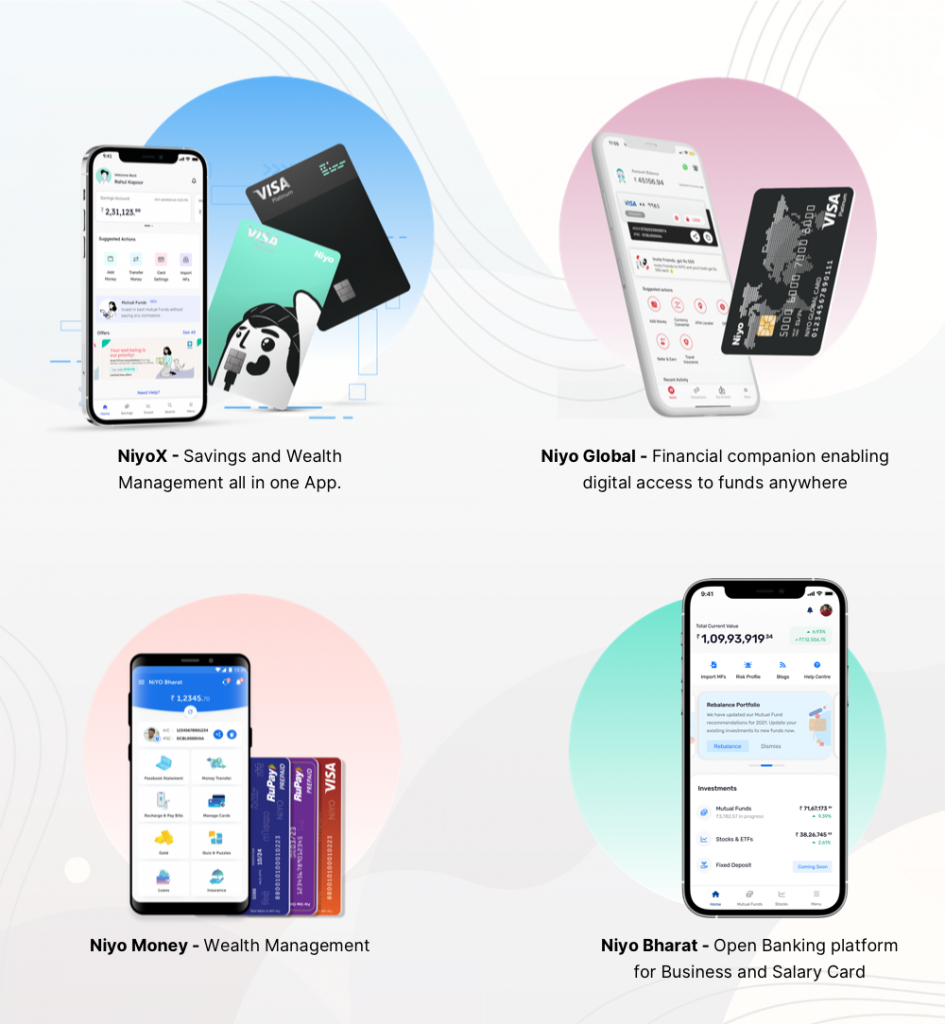

The recent player in the field in India is Niyo, committed to making banking simpler, safer, and smarter through its suite of services. Fintech has partnered with some of the leading banks in the country to revolutionize traditional banking services through technology integration.

At Robosoft, we partnered with India’s first cross-border neobank to create an app that allows users to conveniently operate and spend money across the globe. The app enables users to open and operate a multi-currency bank account digitally and instantly on the app.

Growing Importance of eKYC in Digital Onboarding

In the present times, even though consumers want to engage with a bank, they’re unwilling to visit a branch. The ongoing pandemic has been a major driver of this shift. In such a scenario, businesses that offer a superior onboarding experience and digital services are critical.

At Robosoft, we partnered with India’s first virtual private wealth management platform, to create a seamless UI/UX design for the app to allow for KYC-compliant (Know Your Customer) easy registration and onboarding and Touch ID enabled login.

In Asia, the FinTech market is led by China and India, two economies with already well-established systems of civil identity. WeChat Digital Identity in China and Aadhar in India are leveraged by tech providers to enable eKYC, making the onboarding process frictionless.

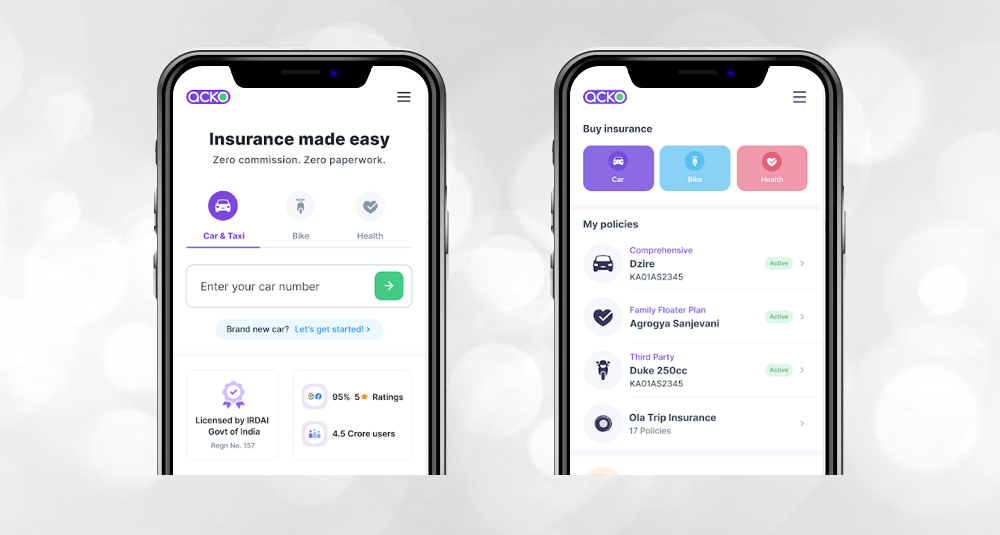

Acko is a fully digital general insurance company based in India. It provides personalized pricing to customers using deep-data analytics. It also studies customers’ behaviors and interaction patterns to suggest insurance products accordingly. Another innovative offering by Acko is Ola Ride Insurance. If you’ve booked an Ola Ride, you can notice a checkbox to insure your ride. The service allows you to instantly secure a cover for lost baggage (including laptops), missed flights, as well as unplanned medical expenses. Pretty convenient, right?

This is an example of embedded insurance that solves one of the biggest problems of the industry – that insurance is sold, not bought.

ACKO Insurance – a single platform for Bike, Car and Health Insurance

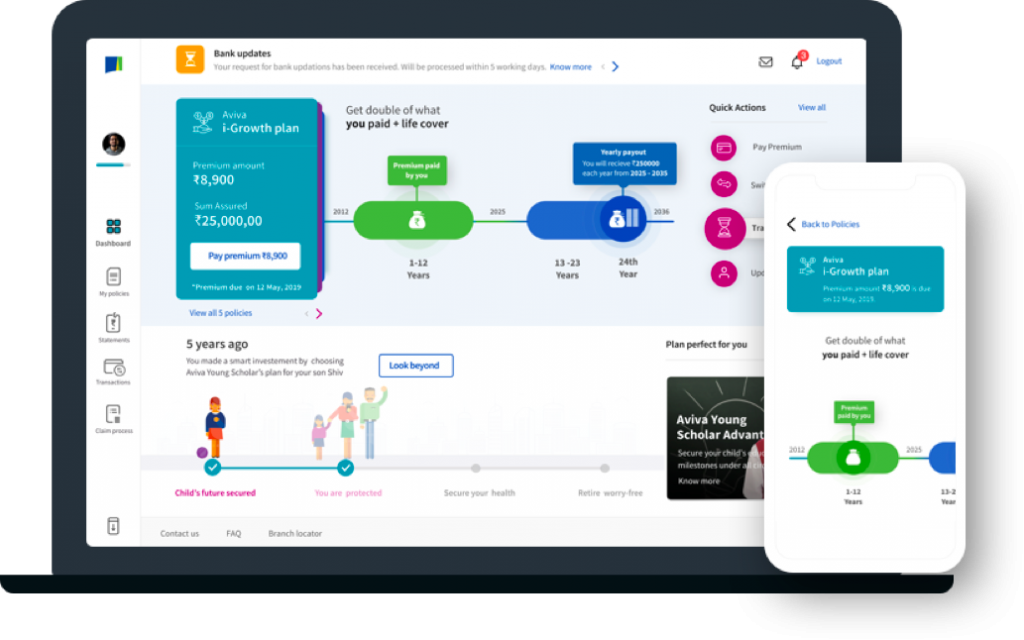

We partnered with Aviva Aviva Life – one of the leading life insurance companies in India, to redesign their website. The website revamp changed the perception about life insurance products by connecting them to the celebration of life instead of being a risk mitigation tool. We created a multi-engaging experience design that was engaging and showcased Aviva’s range of products aligned with individual milestones in a person’s life.

Aviva Life Insurance Web and Mobile Platform

Mobile Peer-to-Peer (P2P) Lending Platforms

Asia Pacific has emerged as a leader in the mobile peer-to-peer (P2P) money transfer market. According to data, Asia Pacific is the home to more than half of the smartphone users across the globe. The availability of low-cost smartphones and increasing disposable incomes in the region have fuelled the popularity of P2P financing platforms. Most governments in the APAC region have also been actively promoting digital payment initiatives, which has helped reduce the costs associated with money transfer (such as UPI in India).

KoinWorks is one of the leading digital lenders in the growing P2P lending space in Indonesia. The FinTech firm has enabled thousands of SMEs to access credit and grow their business through a simple app-based lending platform. In India besides Paytm, players like Phone Pe, BHIM UPI, etc. have become popular.

Alipay and Tencent kickstarted QR code-based payment systems, making mobile payment the most popular payment method in China. Presently, QR code payments have reached Africa, and other countries in the Asia Pacific are rolling out national QR code standards for broad adoption. In the present times, social distancing and personal hygiene have become essential aspects of our lives. In this situation, QR code-based payment systems provided a safe and utterly contactless method for sending and receiving money, which was a great enabler for small businesses in most parts of Asia. During the lockdown restrictions in 2020, India’s 12 lakh robust Kirana retail system drove the cashless revolution in the country. Many shifted to digital payment systems to meet the needs of their customers in a safe and contactless manner. Paytm went a step ahead to launch Paytm SoundBox, a voice-activated POS (point-of-sale) machine for small merchants. Shaped like a small speaker, the SoundBox supported multiple payment methods.

Personalization is the solution to building trust and loyalty for any organization. This is one of the main reasons behind the growing popularity of AI in banking and other FinTech solutions. ML algorithms can help analyze customers’ information and predict the services that would be the most appreciated by them. For instance, Coverfox uses AI-based insights to enable users to compare and choose from a range of insurance plans from various companies.

“Our partnered merchants spend massively on customer acquisition and retention. The last thing they want is losing a customer due to payment failure. We are excited to introduce an AI-based routing engine that addresses this problem by optimising the payment workflows and routing the transaction to best-performing payment aggregator in real time. Further, this will help online merchants reduce development effort to enable various PG providers and achieve faster time to market.” – Puneet Jain, Vice President – Paytm Payment Gateway

The Super App Revolution

Super Apps, the “One app to do it all” concept that became popular in China has now become a global phenomenon.

Paytm, India’s largest mobile payments and e-commerce platform can be safely called India’s first Super App. It allows users to do multiple things like transfer money, buy gold, book tickets, and even make hotel reservations. Presently, Paytm has over 150 million+ monthly active users and the highest market share in offline merchant payments with 15% month-on-month growth. Paytm has also invested heavily in its wealth management and investment portfolio.

‘’There are many lessons to be learned from emerging markets for the U.S. FinTechs, but perhaps the most important trend we’re seeing and could learn from today is the Fintech super app.’’

Lessons from the Asian Fintech Landscape

Here are some key lessons gleaned from the Asian FinTech majors and disrupters that could help you build the next fintech unicorn.

Look Beyond Your Horizons

Ping An, a well-known Chinese FinTech, started as a state-owned insurance company. Today, customers can keep their cash with Ping An’s bank or invest it through Lufax, its wealth-advisory arm. They can also sign up for education services or buy a car and then finance the payments through its consumer credit unit. Lufax also uses a facial recognition tool for account opening, like many other fintech companies in China that are leveraging the power of AI/ML to make digital banking more secure.

Tencent is yet another interesting example in this category. Tencent’s core business is not financial services but social networking channeled through its social messaging platform – WeChat. Using WeChat, Tencent offers users a wide variety of services, such as online shopping, booking taxis, and ordering meals. By integrating these services and designing powerful experiences centered on consumers’ everyday needs, WeChat has gained relevance in users’ daily lives and has almost become indispensable for most Chinese people.

Create a Frictionless Customer Experience

The rise of technology in financial services has thankfully dispensed the need to wait at physical branches to carry out simple monetary transactions. Modern customers are increasingly looking for personalized solutions to manage their money and other aspects of life. For the same reason, payment apps have become exceptionally popular, thanks to the simple and easily navigable UX/UI.

For instance, Piggipo, a Thailand-based app for managing multiple credit cards via one interface, securely monitors spending and helps with scheduling payments, saving money and time. Besides convenience, Piggipo enables users to see their credit card statement in real-time, set spending limits, and view each card’s due date.

Focus on Creating Engagement

WeChat Pay is one of the best-known fintech disruptors from China. At the time of its launch, Tencent used an exciting gamification feature known as digital red envelopes to increase engagement and retention. These red envelopes could be filled with virtual cash or games and sent by users to other groups. The users in a group would then compete against each other to win the red envelope, making the platform highly engaging and adding to its popularity.

Here’s another example from Ant Financial that launched Ant Forest to reward customers using AliPay to pay their bills or perform activities to lower their carbon footprint, such as using public transportation.

Engagement is not just limited to customers. The best solutions come from hiring the best talent in your team. To achieve this, Gojek made a conscious effort to make working in the company an attractive proposition. They encouraged content on platforms like Medium, of their designers and engineers writing about how they solved several consumer problems. By highlighting their employees’ achievements, the company gave an insight into its productive work culture that acted as a hook for attracting more talent.

Increased Focus on Customer-Centricity

Asia is home to a few of the world’s biggest Fintech unicorns, and the venture capitals keep flowing in. Conducive market conditions, including a large number of tech-savvy audiences, along with the disadvantages of the traditional banking model have cumulatively meant that the consumers have been targeted at just the right time. For example, half the population of Indonesia is under 30, and the smartphone penetration crossed 50% very recently. This means consumers are waiting to avail themselves of services through their smartphones and the internet.

Additionally, many of these companies have spent heavily on loyalty and user retention, whether it is through point-based reward systems (Cred), offering discounts and coupons (Gojek), or earning positive equity through various campaigns aimed at genuinely helping people in their times of need (KoinWorks). For instance, KoinWorks launched the KoinWorks Cares program to educate users about safe investment options during the pandemic. They also started a massive donation campaign providing a sizable insurance cover for free to all the donors and used the collected funds to purchase test kits for Indonesian citizens.

In Asia, the appraisal of loan applications, approval, and disbursement have all become simplified. There is no dearth of digital payment options, with giants like Amazon and Google recognizing the potential market for payment in India. Meanwhile, China already boasts three of the highest-grossing digital payments companies in the world. This has also created opportunities in Asia for venture capitalists to fund start-ups that provide FinTech services – something that the US needs to work on. Although the USA has more FinTech startups (5,799) than Asia (2,849), the FinTech deal counts the difference between the two, at the end of 2019 Q3, was 152 (Asia) as opposed to 156 (US).

Uncanny Partnerships Lead to Big Rewards

No business is an island, and cross-industry partnerships could help in optimizing customer experiences across the board. The data interoperability agreement between JD Finance and Tencent is an example. JD uses data from WeChat’s messaging platform to make product recommendations to customers and helps vendors with their products.

The EY Global FinTech Adoption Index 2019 also points to the rise of non-financial services companies such as retailers, technology platforms, and automakers developing their technology-enabled financial services offerings. These organizations have built upon existing relationships with customers to offer holistic propositions accompanied by complementary services, such as insurance and lending that were once the exclusive purview of financial providers, says the report.

Leveraging Emerging Tech to Drive Better Customer Experiences

While the use of AI has become commonplace for Asian FinTech players, many are now dabbling into newer tech like blockchain to disrupt the financial services industry further. While there are only a few examples of companies presently using blockchain in their product or service offerings, technology’s decentralized nature will be a significant game-changer regarding security and speed for fintech companies.

Galileo Platforms, a technology platform company serving the insurance sector in Hong Kong, uses blockchain technology to connect distributors and insurers, enabling them to process real-time transactions. Mai Capital specializes in blockchain and cryptocurrency investments. Their flagship product is the Blockchain Opportunity Fund, a multi-strategy hedge fund deploying quantitative trading and arbitrage strategies.

In Conclusion

The world of financial services has undergone tremendous developments in the past few years. However, a lot of these changes are not attributable to bankers. Instead, people in business, entrepreneurs, and engineers have been chiefly responsible for the FinTech revolution in Asia and beyond. Instead of waiting for the traditional banking industry to evolve, these people took it upon themselves to address customer needs by involving key players.