Last week’s LendIt Fintech event was a great gathering of Banking, Fintech and Lending professionals from across the globe.

Industry experts covered everything from the future of the banking industry in a digital age, to blockchain and the application of AI and machine learning in the financial services domain.

Here is a roundup of some of my key takeaways from the event:

Banking in a post-digital age – being always present for the always-on customer

The banking and the financial services industry is going through a pivotal time. The most critical reason is the changing digital preferences of the always-on customer. Owing to the changing customer preferences and innovations happening in the industry, financial enterprises and banks are compelled to re-imagine the conventional way of connecting with their customers.

Digital is where today’s generation spend a vast majority of their day and the vast majority of their time. An average adult spends about 4 hours a day on the digital platform, checking their smartphone 150 times a day. And, smartphones are not the only connected devices customers are present on – there are wearables, smart speakers, smart cars, smart TVs and the list goes on. It is expected that by 2020 there will be 30 billion connected devices. It is no longer about being present on the digital medium; it is about building a personal relationship with the customers.

As Avid Modjtabai, of Wells Fargo, points out in her talk:

‘It is about developing a profound level of insight into every customer and connecting with them when and where they need us — with experiences that make a difference in their lives.’

Today’s customers share a great deal of information about themselves with enterprises, with the trust that these enterprises will manage and leverage this data to make their lives simpler. This gives enterprises the opportunity to go beyond the transactional relationship with their customers and make it personal.

Banks have to make sure that they are innovating at the same pace as their customers see in other walks of life.

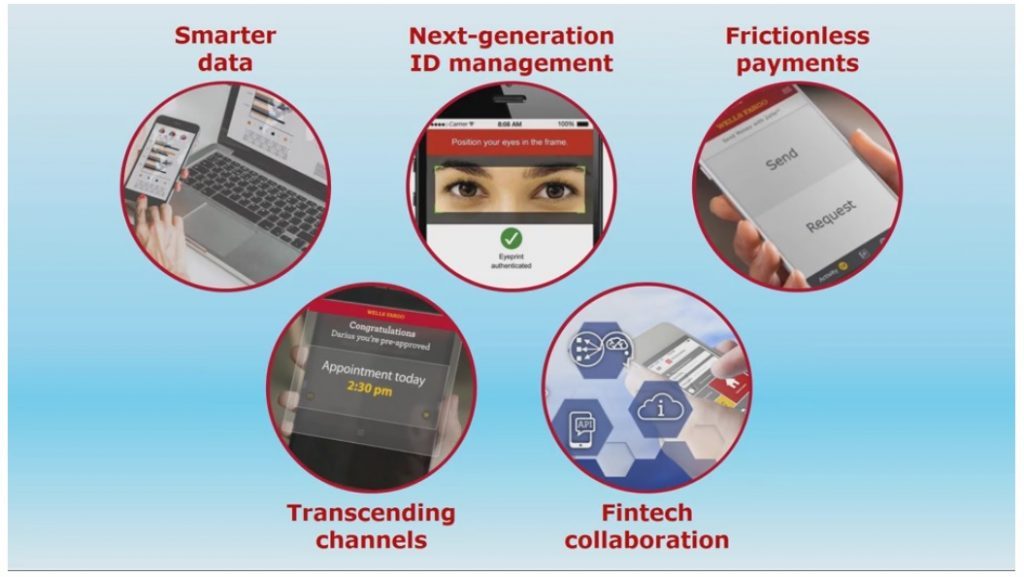

Here are the few ways banks can achieve this:

Image source: Lendit.com

Smarter Data

Enterprises have access to over 375 petabytes of data on customers’ behaviour and preferences. To put that into context, one petabyte can store the DNA information of the entire US population and clone it two times over.

With bigdata, we can make this data work and work harder on behalf of the customers.

According to PwC – 46% of the banking customers are digital-only. This is a huge opportunity for the industry to deliver a contextualized, hyper-personalized experience at the moment wherever they are.

In the future data and AI together can:

- Enable customers to manage their money with just voice.

- Give intuitive tips that would help customers plan their finances.

- Help in underwriting and fraud management.

- Look at the cash flow patterns of customers and give relevant in-the-moment insights.

Next-Gen ID management

Customers trust banks to secure their assets. Identity management is a core component to manage that trust. With customers linking their IDs and financial accounts to a lot more apps and devices, ID management has become more and more complicated and important.

There are about 60 records that are lost or stolen every second, and that adds up to a humongous 5 million records every day.

With a growing number of security and identity breaches, it has become essential for banks to verify every customer at each and every interaction. Today, financial institutions are moving away from knowledge-based authentication to more advanced processes like biometrics, geolocation tracking, device finding technologies, leveraging AI to look at patterns, etc. This combination of technology is making the process much simpler and secure for customers.

Frictionless payments

Technology has transformed the commerce and transactions landscape. Today consumers want their transactions to be integrated and seamless and expect the payments’ process to be done in the least possible steps.

Technology has reinvented commerce. For instance, in Sweden, cash accounts for only 2 percent of all the payments and half of Swedish bank branches are cashless today.

It is imperative for industries to develop simpler and fast-moving money movement capabilities and experiences. Banks have the capability of being pioneers in this area, and some are raising the bar higher, e.g. Zelle P2P payments from Wells Fargo, helps customers transfer money between participating bank accounts in real time.

Transcending channels

Today customers are always connected, and they expect that from enterprises they deal with as well. Customers want to talk to their banks in the moment of their need – this model is changing the way financial institutions have been thinking about channel and distribution.

Also, banks have to make sure that they are not just available when the customers need them; they also give the customers the choice of communicating with them in the way they wanted, e.g., Apple announced Apple business chat with Wells Fargo. It enables customers to chat with their banks through the same messaging app in which they are talking with their friends and family.

Fintech collaboration

Today technology is not just an enabler but is a differentiator for enterprises across industries. And, hence Fintech collaboration is becoming increasingly important for banks. In the coming years, most product innovations will come from fintechs and banks working together.

Finding the right ‘Product Market Fit’ in Fintech is important:

In this digital era, Fintech is more about the ‘Fin’ and less about the ‘Tech’. A lot of financial enterprises build products with ancient infrastructure with a thin layer of UI on it. It is important to find out the right Product Market Fit in Fintech. Instead of looking for a market first, enterprises should aim at finding out the problem that they are going to solve, build a great product around it and then focus on consumers where the product is a right fit.

Here are few tips from Andy Rachleff, co-founder and executive chairman of Wealthfront, to make sure that you find the right Product-Market-Fit:

Understand the What, Who and How before building a product

Three crucial pillars of building a great technology product are finding the answers to these three aspects:

- What – what are you going to build?

- Who – for whom is it relevant?

- How – what is the business model?

Most enterprises do not realize that they shouldn’t iterate on the ‘What’ too much. It is essential for entrepreneurs to identify an inflection point in technology and build a great product around it and then identify the market that needs the product.

Be unconventional

Trying to do better what someone else does is a path to mediocrity. In a technology-led industry, it is important that enterprises innovate and create differentiation for themselves.

Customer delight is the greatest form of advertising

In the journey of product-market fit, paid advertising and customer acquisition can mislead enterprises into thinking that their products are doing well when in reality they aren’t. Further, advertising is a fixed cost, and for small and medium-sized enterprises it means investing in that fixed cost hoping that the market is big enough to take care of that fixed cost. Enterprises should aim at exponential and organic customer growth and invest in infrastructure and build a robust technology first. A great product will delight customers, and that will ensure word of mouth and organic growth of customers.

Not every product idea will work

It is important for enterprises to realize that not every product idea works, some of them are bound to fail. However, it is critical to identify the ones that work and doing all that you can to make those successful.

Bitcoin and cryptocurrency – a vision for the future

In January 2009, the Bitcoin network came into existence with the release of the first open source Bitcoin client and the issuance of the first Bitcoins, with Satoshi Nakamoto. Since then, the number of businesses accepting Bitcoin continues to increase, and along with it, the industry expectations on the currency continue to be bullish. In fact, even the Mt. Gox fraud of Bitcoins, led to just a drop of 15% in the value of the currency.

How Bitcoin will change the future of banking

The transactions that happen beyond the medium of the banks mostly remain unbanked. Bitcoins can help in bridging this gap and make the unbanked transactions a part of the real economy. Further, Bitcoins help the movement of the currencies easily from one country to another without the need to convert it. Also, it is easier to catch fraud if a transaction is happening via Bitcoins.

Governments across the globe will recognize Bitcoins’ potential

There are a lot of regulatory issues around Bitcoin as of now. However, in the coming few years governments will make it easier for the people to deal with Bitcoins since governments compete for money, entrepreneurs and people, e.g. South Korea made Bitcoins illegal and then they realized that 40 percent of their population already has a Bitcoin wallet, so they had to ease out their regulations. Since the regulatory requirements are not so stringent in the developing economies, they are a potential market for Bitcoins.

Bitcoins will be the new normal

While established financial and payment enterprises aren’t supporting Bitcoins since they already have an established system, companies like Coinbase will become the banks of the future.

Applying AI and Machine Learning to Financial Services Using the Google Cloud

In 2010, Deepmind a start-up created a neural network that learns how to play video games in a fashion similar to that of humans and Neural Turing machine.

Google foresaw how neural networking and AI would change the future of technology forever and acquired the company in 2014. They started experimenting with this technology and reinvented how Google works internally. Initially, Deep Learning was used in image recognition through Google photos. In 2015, the technology advanced to not just recognize the targeted image but also the environment (or pixels) around it and further change it.

Image source: Lendit.com

In the coming years, the technology was used for reading and writing through an auto response to Gmail and voice recognition.Today Google is using AI and Machine Learning to identify user behavior patterns and give output accordingly on Google’s ad network.

Image source: Lendit.com

How AI and Machine Learning can change the financial services landscape

Machine Learning can ingest a humungous amount of customer data, structure it, process it and convert it into tensors. These tensors can be then used to train a machine learning system and deliver customized results.

Image source: Lendit.com

Financial services can use these techniques of Machine learning and AI to

- Analyze their customer lifetime value (CLV) better.

- Define where enterprises can target campaigns to engage most with their customer set.

- Prioritize customer interaction based on the CLV.

- Build more efficient processes by using the technology see and fill forms; and also work on quality assurance processes.

- Read documents and analyze compliance with documents.

- Listen and speak to customers and shorten the time from enquiry to resolution.

The emergence of the Internet of Value

The Fintech space is evolving very fast. With technologies like blockchain coming up, the fundamental shift that is expected to happen in the coming few years is the emergence of Internet of Value.

This means that financial assets and money will start moving as efficiently as data has been moving in the last 25 years.

The biggest change that blockchain will bring is the complete inter-operability between all the money, systems and the ledgers of the world.

Correspondent banking will dissolve

Today, if someone wants to transfer money across the globe, they have limitations of taxes and time. This issue becomes more prominent when the transaction amount is smaller. Technologies like blockchain will bridge this gap.

Interoperability of data will fasten the pace of globalization

There are three main keys to achieving true Globalization

- Interoperability of data

- Interoperability of good

- Interoperability of money

While we have been able to achieve the first two, we are still lagging behind when it comes to interoperability of money. Blockchain will help in achieving this. The interoperability of money will also be followed by the emergence of IoP or Inter ledger protocol, which is IP or standardization process for ledgers.

Convergence of technologies will make Fintech simpler

The number of smartphone users has been rising and will continue to grow in the coming years. According to the World Bank, in the coming few years every adult in the world will have a digital bank account on their smartphone.

Today, there is the technology and the device, however finding out a link that will wire all of this together is missing. In the coming years, the Fintech industry will figure that out through the interoperability of monies.

Regulators are supporting systems that make sense

Governments across the globe are working towards inclusion of the people and developing economies which are not connected to the world economy today. Digital currencies and enabling regulations by these governments will help in achieving that. Most payments will be machine to machine once the interoperability and developing world problem is solved.

Data security and privacy will be of utmost importance

As the demand for digital assets grows, governments will also make sure that data privacy issues are addressed. New and stringent laws will be introduced. California consumer privacy act is coming out this year and EU GDPR privacy laws etc. are some steps in this direction. We are in the best of Fintech regulatory environment right now.

Currencies will have more use cases and will be more liquid

ICOs are problematic because currencies need to be as liquid as possible and have as many use cases as possible.That will drive value and utility. The early beta of this is cross-border payments but this is just the beginning, and we will see more such use cases of currencies coming up.

Conclusion

The banking and the financial services is at a turning point right now. This year’s LendIt conference gave us a detailed view of the future the industry is moving towards. With changing customer behaviour, technology advances and innovations there lies exciting times for the industry ahead.

You can find more about the event here.